The continuing blockade of the Strait of Hormuz, announced by Donald Trump on April 12, has made it more difficult for Iran to sell its energy resources, and buyers are struggling to find alternatives due to the shortages, with the European Union already experiencing a “black April,” in the words of IEA head Fatih Birol. The Kremlin’s position appears favorable amid the ongoing crisis, but Moscow will not be able to enjoy the windfall for long, writes George Voloshin, an international expert on sanctions and the study of post-Soviet countries. Russian oil exports are already facing both cyclical and structural challenges.

Доступно на русскомContents

“We are entering a ‘black April.’ In the Northern Hemisphere, where we are, April usually marks the beginning of spring, but today, I fear it will mark the beginning of winter,” Fatih Birol, head of the International Energy Agency, told French newspaper Le Figaro on April 6.

He called the current crisis the most serious supply disruption in the history of the global oil market, more serious than the crises of 1973, 1979, and 2022 combined. The International Monetary Fund (IMF), which in January had forecast global growth of 3.3% in 2026, is revising its projections downward. IMF Managing Director Kristalina Georgieva warned of the asymmetric effects the crisis will have on poorer, energy-importing countries and said that “even in the best case, there will be no neat and clean return to the status quo ante.”

The European Union entered the Iran crisis burdened by two problems: on the one hand, heavy dependence on imported energy resources; on the other, limited room for fiscal maneuver after the COVID-19 pandemic, the 2022 energy shock, and sharply increased military spending over the past four years.

Speaking before the European Parliament’s committee on economic and financial affairs, European economy commissioner Valdis Dombrovskis warned that even if a ceasefire in the Middle East holds, GDP growth in the EU for 2026 will still fall by 0.4 percentage points, while inflation will rise by 1 percentage point. If fighting resumes, the hit to economic growth will total 0.6 percentage points, while price growth will increase by a full 1.5 percentage points. “[It is] clear that we are facing a stagflationary shock,” Dombrovskis said in an interview with the Financial Times.

The European economy risks facing a stagflationary shock if the war in the Middle East drags on

For now, the second, less optimistic scenario appears far more likely. To understand why, it is enough to look at conditions in the fuel market.

Ryanair CEO Michael O’Leary said the carrier would be forced to consider canceling some flights and cutting capacity this summer if fuel shortages continue.

ACI Europe, the airport industry group representing more than 600 airports handling over 95% of the EU’s commercial air traffic, sent a letter to European commissioners on April 9 with a blunt warning: if transit through the Strait of Hormuz does not resume on a stable basis within the next three weeks, a systemic shortage of jet fuel will become a reality.

The specific deadline is the beginning of May — the height of preparations ahead of peak summer traffic. Some EU member states have jet fuel reserves sufficient for only eight to 10 days, reported Italian daily Corriere della Sera, citing sources among EU jet fuel suppliers and airlines.

Some EU member states have jet fuel reserves sufficient for only eight to 10 days

Air transport generates 851 billion euros in GDP and supports 14 million jobs in European economies. A physical fuel shortage is not an abstract price risk but a direct threat to the entire sector.

Passenger aircraft at Brussels-Zaventem Airport (BRU) in Belgium

Dombrovskis reminded lawmakers that during the previous energy crisis, governments spent about 1% of GDP on non-targeted price subsidies and fuel tax breaks. This time, the European Commission insists, support must be targeted, temporary, and moderate. VAT on diesel can be cut for a quarter, but not for a year — and only if the benefit reaches transport operators rather than getting trapped in hedge funds. In any case, high debt and high interest rates leave only a narrow corridor for maneuver.

Despite signs of a deepening crisis, there is little reason to expect the European embargo on Russian oil supplies, in force since late 2022, to be lifted. In January, a ban took effect on imports of petroleum products made from Russian crude in third countries such as India and Turkey, and after the outbreak of the war in Iran, the European Commission stated in no uncertain terms its principled opposition to making up for lost supply through the use of Russian sources.

The crushing victory of Hungary’s opposition in the April 12 parliamentary election was also significant, as it removed the main obstacle to the 20th package of sanctions against Russia, which Viktor Orban’s government had blocked in February. One provision in that package is a full ban on European companies providing maritime transportation services for Russian oil to third countries, replacing the more flexible price cap.

At his first news conference, Hungarian opposition leader Peter Magyar acknowledged that Budapest’s dependence on Russian energy resources would remain for some time, but he also stressed the need to diversify supplies.

More broadly, the Middle East crisis appears likely to give fresh momentum to calls in Europe for diversification, wider adoption of renewable energy, and a parallel reduction in hydrocarbon consumption.

Unlike Europe and other major importers, Russia is actually benefiting from the Strait of Hormuz crisis — for now. Unexpectedly, the blockade has turned Russian oil from a toxic asset into a sought-after and liquid commodity, one for which U.S. sanctions were even temporarily eased. India increased imports of Russian oil in March to their highest level since June 2023, and the Philippines bought ESPO crude for the first time in five years.

Clearly, the spike in interest is the result of the absence of obvious alternatives, meaning once prices normalize, demand will fall. The U.S. Treasury has extended General License GL 134A to cover Russian oil loaded onto tankers before April 17, but it is not clear whether a new extension will follow that update.

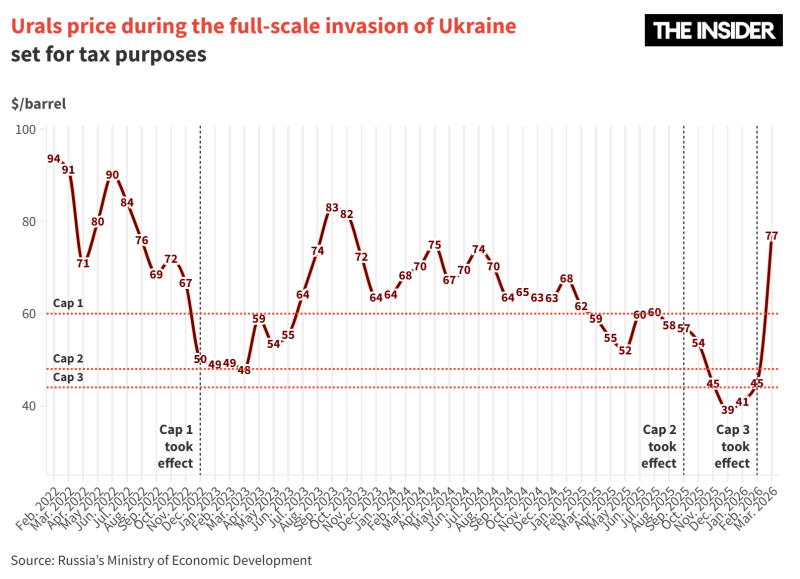

Still, the crisis has come at a particularly opportune moment for Russia’s increasingly strained budget. In the first quarter of 2026, Russia’s oil and gas revenues fell 45.4% year-on-year. The country’s federal budget deficit for January through March totaled 4.58 trillion rubles, already exceeding the planned figure for the full year. The average price of Urals crude used by the Finance Ministry for tax purposes fell in February to $44.59 a barrel, against a budget benchmark of $59.

March reversed the downward trend: Urals rose to $77 a barrel, and April revenues (which are calculated based on March data) from the mineral extraction tax alone could reach $9 billion, or about 700 billion rubles, according to Reuters, twice the level seen in March. However, it is unclear how long high prices will hold, and Russian authorities still have few reasons for optimism in the medium term.

First, persistently high oil prices over a long period would increase recessionary pressure in importing countries, including in the world’s largest economies. That would inevitably lead to a fall in overall demand and, accordingly, falling prices themselves. For example, it took Brent’s spot price from early September 2008 — about $100 a barrel — two and a half years to return to its previous levels.

Second, both the expected and already partly realized deficit in Russia’s federal budget is so large that excess revenues earned over just a few months clearly will not be enough to cover it. In particular, planned spending this year on defense, national security, social policy, and debt servicing totals 27.8 trillion rubles out of a 44.1 trillion-ruble budget. Those items cannot be cut, which helps explain why the Economic Development Ministry projects a deficit budget through 2042.

The deficit in Russia’s federal budget is so large that excess revenues earned over just a few months clearly will not be enough to cover it

Third, the structural weakness of Russian oil exports after 2022 lies not in physical volumes (which will be discussed below), but in the gap between price and actual revenue. Before the full-scale invasion of Ukraine, Urals traded at a discount to Brent of $1 to $2 a barrel. In 2024 and 2025, that gap was about $15. And after British and U.S. sanctions were imposed against four of Russia’s largest oil producers and exporters — Rosneft, Lukoil, Gazprom Neft, and Surgutneftegas — it exceeded $20 a barrel in some transactions.

Since the beginning of March, the discount has been either minimal or even negative —meaning Urals has traded at a premium to Brent — but that is a temporary result of the high prices caused by the current shock. As long as Russia and its “shadow fleet” remain under sweeping Western sanctions and embargoes, downward price pressure on Urals will persist.

The Economist has also reported that tankers in Russia’s “shadow fleet” lose 30% to 70% of their productivity after sanctions are imposed, sharply increasing transaction costs. According to estimates by the KSE Institute at the Kyiv School of Economics, sanctions caused $166 billion in losses to Russian oil exports from March 2022 through November 2025. At the same time, sanctions did not undermine physical shipment volumes: crude oil exports in 2025 totaled about 4.8 million barrels a day, virtually unchanged year over year.

Fourth, Ukrainian strikes on Russian port infrastructure have exposed a vulnerability that Western sanctions failed to create over all these years: the physical blocking of exports. By March 25, about 40% of Russia’s oil export capacity — around 2 million barrels a day — had been temporarily knocked out. As a result, shipments of naphtha from Ust-Luga fell 74% in the final week of the month.

Reuters described the development as the most serious disruption of oil supplies in Russia’s modern history. The strategic significance is clear: Kyiv is depriving Moscow of the ability to monetize favorable price conditions precisely at the moment when they are most advantageous — even if, by early April, half of that degraded capacity had been restored.

Kyiv is depriving Moscow of the ability to monetize favorable price conditions precisely at the moment when they are most advantageous

It is difficult to say whether Ukraine will be able to inflict comparable damage on a regular basis. Given the scale of the recent attacks, the Russian side will of course try to strengthen defenses at key infrastructure sites. But Ukraine now certainly knows which targets it needs to strike first.

In the longer run, a sustained Urals price anywhere below $50 a barrel would be painful for Moscow economically. In the event of a global recession or de-escalation in the Middle East, Brent could return to $55 to $60 a barrel, and Urals, with its usual discount, would end up in the $35 to $45 range.

According to calculations published last year by Re:Russia, under that scenario the budget deficit would reach 6 trillion rubles, or 3% of GDP, instead of the planned 1.6%. Financing that gap would require either borrowing at the central bank’s double-digit rate, or simply issuing more money. Both options are toxic for an economy where food inflation already exceeds 20%.

According to Bloomberg’s calculations, exports of Iranian Light crude were bringing Tehran about $139 million a day in March. Stable shipment volumes, combined with a jump in prices and a sharp narrowing of the discount to Brent (from more than $10 to just $2.10 a barrel) gave Iran roughly $25 million a day more in revenue than it was bringing in during the month of February.

While competitors stood in line at the closed gates of the Strait of Hormuz, Iranian tankers were passing through it without obstruction. But Iran faces the same structural limitations as Russia. Persistently high prices accelerate recession in importing countries and inevitably suppress demand.

Even under current conditions, Iranian oil is sold mainly to China’s independent refineries — the so-called teapots — which traditionally buy more than 80% of Iran’s exports. This is a buyer’s market with hard pricing leverage.

Once global prices fall, the structural discount will return to its previous levels. For decades, Iran has offered buyers substantial discounts in order to sustain exports. To evade sanctions, it has used a range of schemes, from ship-to-ship transfers in neutral waters with AIS transponders switched off to payments routed outside the U.S. financial system. The transaction costs associated with those methods exert downward pressure on Iranian oil profits in the same way the costs of Russia’s “shadow fleet” lower Russia’s revenue from the sale of Urals.

There is, however, a fundamental difference: Iran’s “shadow” exports are physically dependent on a geographic chokepoint that Tehran itself decided to use as a weapon. The Strait of Hormuz is both a lever of pressure and a bottleneck for Iran’s own supplies.

Iran’s “shadow” exports are physically dependent on a geographic chokepoint that Tehran itself decided to use as a weapon

The crisis shows no sign of abating. Talks in Islamabad on April 12 broke up after the U.S. delegation, led by Vice President JD Vance, spent almost a full day failing to secure Iran’s agreement to abandon its nuclear program and meet the White House’s other demands. As a result, Donald Trump announced a naval blockade of the strait, and since then, the passage of dozens of ships has been blocked. Strikes on Iran’s oil infrastructure have not yet become a priority for Washington, likely because they would drive prices even higher. But the military logic of the conflict makes that scenario increasingly less hypothetical.